TETRA Technologies: A Diamond In The Rough That Can Triple In The Next Year

This article was recently published on Seeking Alpha. It might be of general interest to this community and, of course, I would be interested in any comments that might help to prove or disprove my thesis.

TETRA Technologies: A Diamond In The Rough That Can Triple In The Next Year

Summary

- Tetra Technologies, Inc. (TTI) is a deeply undervalued small cap energy services company that will not stay so small and undervalued for long.

- Excluding its controlling investment in CSI Compressco (CCLP), the stock sells at an enterprise value multiple of just 4.0x run-rate EBITDA, despite strong free cash flow generation and growth prospects.

- The company's breakthrough new CS Neptune completion fluid has a multi-billion dollar market opportunity ahead of it, with >80% EBITDA margins, no competition and long term patent protection.

- The company recently signed a joint marketing and development agreement with industry leader Halliburton to distribute this product globally.

- TTI stock can double just to get to the low end of my fair value range. Over the next year, it can triple and more.

TETRA Technologies, Inc. (TTI) is a smallish company that’s been around for a long time. Until recently, it has been an unremarkable company, sort of both everywhere and nowhere at the same time. As I will explain in this lengthy article, I think that is about to change in a big way.

Against its most recent closing price of $3.65, I think the stock is easily headed into the teens over the next year or two. I think this is a stock to own right here, right now, because not only is it extremely cheap but I think perceptions could begin to change rapidly starting with the upcoming Q3 conference call.

INTRODUCTION

TETRA is an oil and gas service company now focused squarely on three businesses: high technology completion fluids, which will benefit from both increasing shale drilling and, particularly, the accelerating recovery in deepwater drilling; water and flowback services, which will benefit from the increased importance of water management in shale drilling; and compression sales and services, in which it participates through its ownership and control of CSI Compressco, LP (CCLP), a separate publicly-traded MLP.

As I will explain, I think that TETRA is well positioned to assume a position of technological leadership in both the completion fluids and water management businesses. Its investment in CSI Compresso is valuable, but in my opinion, may ultimately be a candidate for divestiture.

INVESTMENT THESIS

Over the last year, TETRA has quietly and remarkably transformed itself into a focused company with the potential for market leadership in two large and growing oil services markets: completion fluids, where it has a blockbuster new ultra-high-margin product; and water and flowback services, where it is the number two provider of such services nationwide.

Over the past year, the company has sold divisions, shed liabilities, and reduced and refinanced its debt. Where the “old” TETRA was a bit of a mish-mash with no particular corporate logic; the “new” TETRA is a highly focused company with a coherent and well-defined corporate strategy. In my opinion, the new TETRA is a winner—a long-term growth story that can double over the short term and triple or quadruple beyond that.

While I am bullish on energy related stocks, most of them are highly cyclical and inextricably tied to the commodity price. TETRA has a unique set of secular growth drivers that most other energy stocks do not have.

Investors haven’t yet taken notice, but I think they are about to. TETRA last closed at $3.65, at the lower end of its range over the last year. While analyst targets are in the $6 to $8 range, I conclude a value between $8.38 and $13.09 per share.

MAY 31, 2018: TETRA HOLDS AN “INVESTOR DAY” CONFERENCE

On May 31, 2018, TETRA management held an “investor day” conference in New York City in which the CEO, CFO and the heads of all their divisions gave lengthy presentations and answered questions. This may be the first time this company has ever hosted such an event. Certainly, it is the first time in recent memory.

I think the best way to analyze this investor day is in terms of human nature. Hosting an investor day is a lot like hosting a dinner party to celebrate your new house. You wouldn’t be doing it if you didn’t feel proud of what you had accomplished and where you were headed. It is a sign that management is both excited by their prospects and confident they can deliver. It may also be a sign that they think their stock is a real opportunity.

I was very impressed with the company’s 117-page analyst day presentation. Clearly, a lot of thought and effort went into this presentation. Not only did management explain their business and corporate strategy coherently, they put forth explicit 2018 guidance for each of their business units. I don’t think they would have done that unless they were confident the could deliver at least as much as they promised. In fact, on their earnings call just two months later, they already began raising guidance, however modestly.

I have been following TETRA closely since their investor day presentation. At the time, I didn’t see any need to rush out and buy, but I’ve recently changed my mind. I think the time to buy is now, in front of what I think will be strong Q3 earnings and a meaningful upward revision to Q4 guidance. As well, I think 2019 is shaping up to be a breakout year.

Nobody knows a company better than its own management. But, for obvious reasons, management cannot tell us everything they know. Looking back on the investor day presentation, and what has happened since then, I am convinced that management likely has in store a string of important positive announcements that will cause investors to fundamentally revalue the company significantly higher.

SINCE INVESTOR DAY

Since the investor day, the company has made three important announcements.

First, the company announced a joint marketing and development agreement with Halliburton (HAL) for its revolutionary new CS Neptune completion fluid. Halliburton is one of the global leaders in drilling and completions fluids and controls about a quarter of the market. Driven by Halliburton's global reach, I think revenue and profits from this single product alone can cause the stock to at least double over the next year.

Second, the company reported very strong Q2 revenues of $260 million (versus analyst estimates of $238 million) and earnings per share of $0.04 (versus analyst estimates of $0.01).

Third, the company raised both 2018 revenue and EBITDA guidance, although by not nearly as much as the Q2 outperformance would suggest.

TETRA will report Q3 earnings in early November and I expect that it may represent a critical inflection point in how the company is perceived by investors. I expect the company will report a strong quarter and raise Q4 guidance, perhaps substantially. Management may also give a preview of 2019 guidance.

FLUIDSDOC: CREDIT WHERE CREDIT IS DUE

Before I begin, let me give credit where credit is due. Fellow Seeking Alpha contributor, Fluidsdoc, has been writing about TETRA for more than the past year, and it is their enthusiasm for their new Neptune completion fluid product that initially drew me in. According to their Seeking Alpha profile, they are an industry expert.

Now, Fluidsdoc has been recommending TETRA for the past year and, frankly, they have been early. As I will explain, they connected the dots between what happened in 2017 and what will happen in 2019 and beyond far faster than the market, which in fact still hasn’t connected those dots. That’s often what happens when you know too much and that’s a large part of the opportunity in TETRA today.

When it comes to completion fluids, Fluidsdoc is the ultimate industry insider. I’m pretty sure they are going to be right on TETRA. Even if they are only half right, this will be a very rewarding stock.

Let’s now go through each of TETRA’s operating divisions.

COMPLETIONS FLUIDS & PRODUCTS

TETRA’s Completion Fluids & Products division is an industry leader with a greater than 30% market share for high value fluids. When transitioning from drilling a well to completing a well, completion fluids are used to displace the drilling mud while keeping downhole pressure intact. If you want to know more about the technical details of these fluids, I urge you to read Fluidsdoc’s many articles. They are the real thing when it comes to understanding the science and application of these fluids.

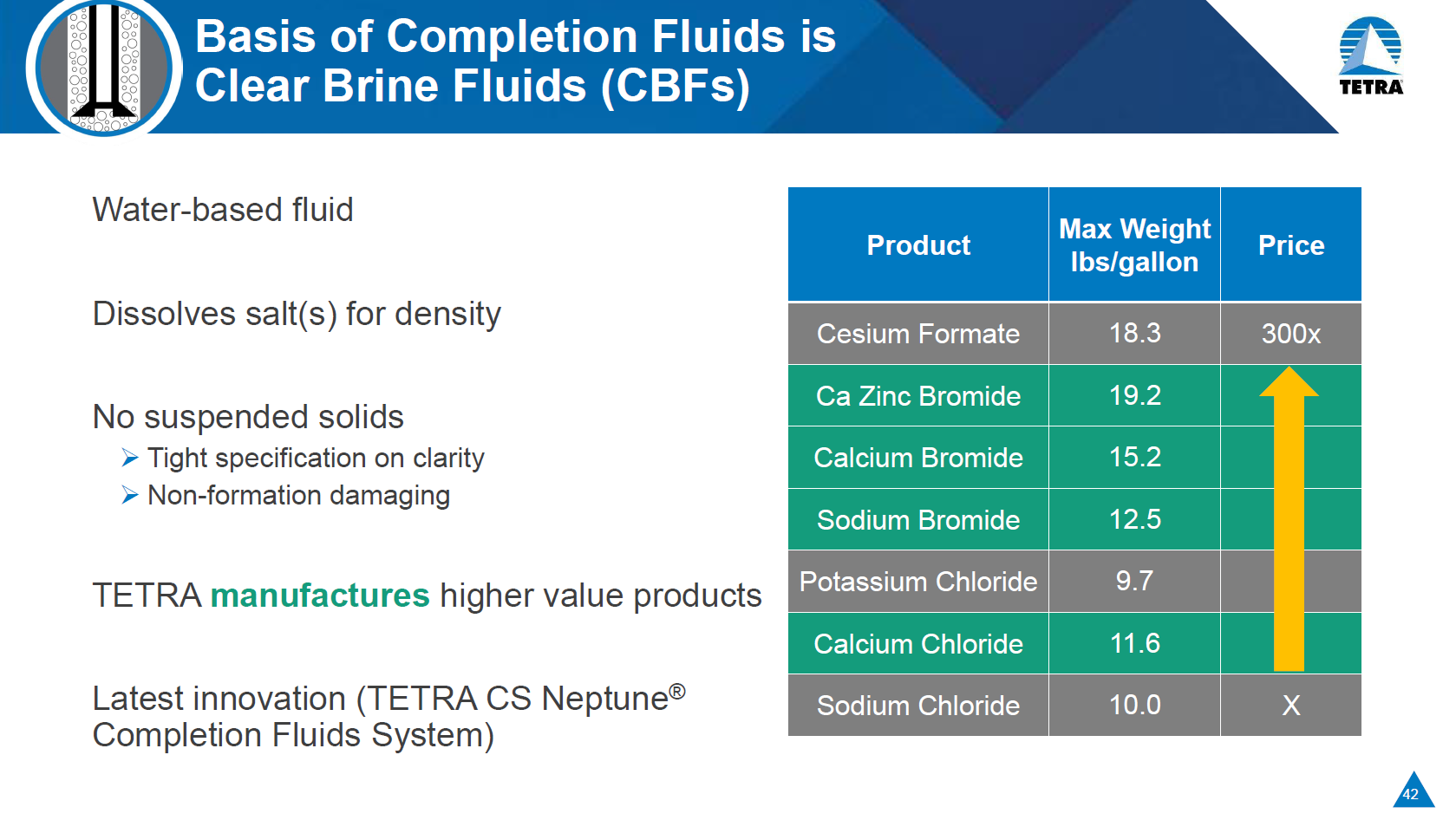

For the purposes of this article, suffice it to say, if you are completing a well, you will need completions fluids. Depending on the type of well you are completing, the fluid you will use can range from a relatively low-cost commodity fluid like calcium chloride for a typical shale well to a very expensive and highly engineered fluid using hazardous or even rare elements for a high-pressure, high-temperature deepwater well.

Source: Company presentation

While TETRA provides fluids for both onshore and offshore completions, what is really driving my excitement is their new CS Neptune product for the complex and expensive wells in the deep waters offshore. This is where the big companies spend the big money and a single project can run into the many billions of dollars. Every well that uses the company’s Neptune completion fluid can add millions to the bottom line. That’s a lot for a small company like TETRA. (With 126 million shares outstanding, each well can potentially add a couple of pennies of EPS.)

As Fluidsdoc explains, there have traditionally been two alternatives for deepwater completion fluids. The first, zinc bromide, is extremely toxic, bio-accumulates in the food chain and is a known teratogen, meaning it causes fetal malformation. These health, safety and environmental issues are real. The U.S. has classified zinc brines as "marine pollutants" and they are prohibited from use in the North Sea altogether. The second alternative, a cesium formate based brine, does not have the same environmental risks, but is extremely expensive and its use frequently difficult to justify. A cesium formate based completion fluid can cost up to ten times as much as a zinc bromide fluid.

In sum, what TETRA has done is to develop a revolutionary new zinc-free completion fluid which is far superior to what exists today. Because it is zinc-free, it has none of the health, safety and environmental issues associated with a zinc bromide fluid; and because it uses no cesium formate, its cost is very reasonable.

According to Fluidsdoc, both Schlumberger and Halliburton, the two leading completion fluids companies, have been working to come up with a zinc-free alternative. They have been unable to do so and, as they write,

Tiny TETRA was about the last company that anyone expected would come up with a solution to one of the completion fluids industries most vexing problems, zinc bromide. But, solve it they did, thus registering the first significant advance in heavy brines technology since they were introduced in the early 1970's.

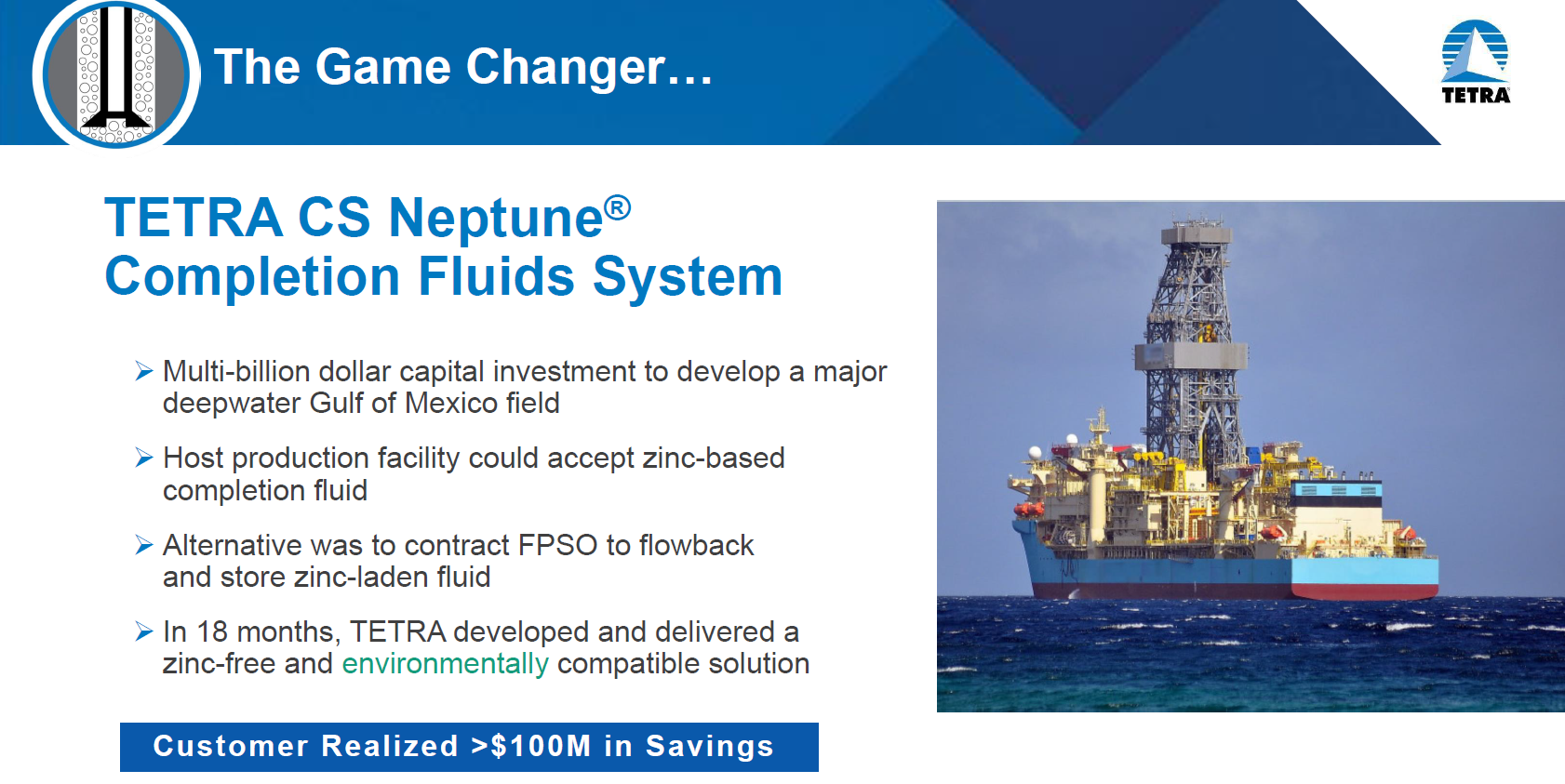

According to the company, CS Neptune was developed for use in a multi-billion-dollar investment deepwater well in the Gulf of Mexico. Had a zinc-based fluid been used on this project, a separate FPSO (floating production storage and offloading) unit would have had to be contracted just to dispose of the zinc-laden fluid. In other words, the E&P company would have had to hire one of these (as in the picture below) just to dispose of the contaminated fluid.

Source: Company presentation

Source: Company presentation

All-in, the use of CS Neptune resulted in savings of greater than $100 million. That’s a huge savings and explains why this product can command such high margins.

According to the company’s 2017 annual report,

The success of the TETRA CS Neptune® technology project simply cannot be overstated. In 2017, TETRA completed a multiyear project in the Gulf of Mexico that, by all measures, was an unqualified success. We view the TETRA CS Neptune® completion fluids system as a transformational, disruptive technology that is generating additional interest from customers around the world. We are excited about the future and about the role TETRA CS Neptune® technology will play in the growth of our Fluids Division.

(Emphasis mine.)

The critical question is, is this true or is this just so much corporate puffery? This is where Fluidsdoc comes in.

This the first major advance in halide fluids in 40-years [] and enables operators to conduct completion operations without the risk of zinc, or cost impact of cesium formate. That's why I am confident that TETRA will win some of these markets for Neptune CS. They already have a strong presence in Brazil and the North Sea and Africa, leaving only the Far East-China, Vietnam, and Malaysia for expansion.

And,

TETRA is going to get business that used to go to [zinc bromide] with all its attendant risks, or cesium formate with its high cost structure. Every well they use it on in deep water is worth millions to its bottom line.

If so, that’s enormously consequential from a financial perspective.

Let’s take a look at the potential financial impact of Neptune on the company. Source: Company filings, author's calculations

Source: Company filings, author's calculations

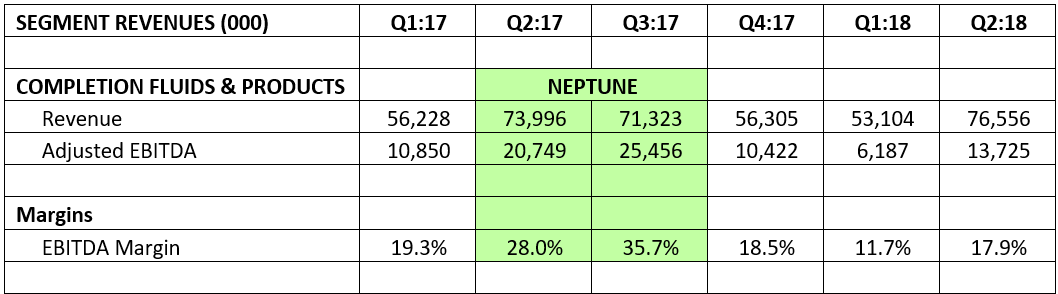

Neptune is a product in its infancy. In Q2 and Q3 of 2017, TETRA provided Neptune completion fluids for a major Gulf of Mexico project. While this was not the first well that Neptune was used on, it was the first truly large-scale application of Neptune on an ultra-high-value well. What we don’t know is exactly how much revenue and EBITDA were generated by this project. But we can guess. Just looking at how both revenue and EBITDA popped during those two quarters (and also taking into consideration the typical seasonal strength in Q2) suggests that this single project generated in the range of an incremental $20-25 million in revenues at an EBITDA margin of at least 80%. That really made me sit up and take notice.

There are two important takeaways here. First, if Neptune gains traction, it can drive an enormous amount of profitability with virtually no incremental capital investment. Second, Neptune earnings deserve a high multiple and can catalyze a fundamental revaluation of the company.

So, the next question is, how big is this market?

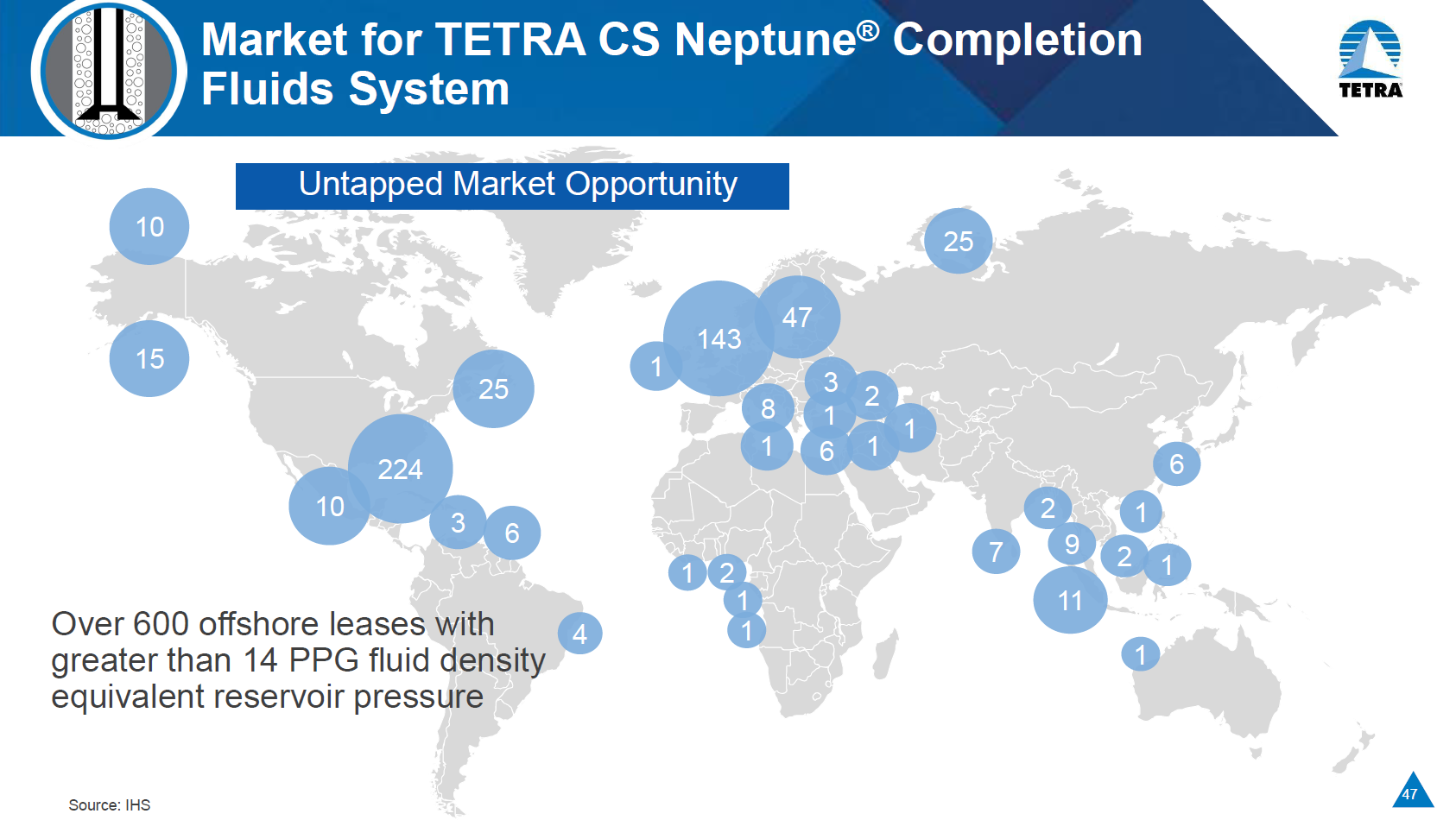

According to the company, there is an untapped market opportunity of over 600 offshore leases with wells that could benefit from CS Neptune. As shown below, 143 of these are in the North Sea, where Norway has banned zinc-based fluids for environmental reasons. Another 224 are in the Gulf of Mexico, where TETRA has already proven the success of Neptune.

Source: Company presentation

Source: Company presentation

Using the company’s estimate of 600 wells, at an average of $5 million per well, would suggest a $3 billion revenue opportunity. (Recall, that a single large project can potentially generate up to $20-25 million in revenue, so this estimate may be conservative.) At an 80% margin that’s close to a $2.5 billion profit opportunity. That’s a lot of opportunity for a small company like TETRA.

In its investor day presentation, TETRA disclosed that it wanted to partner with a “global drilling and fluids market leader” to enhance its distribution and service capabilities for Neptune. That’s actually a tall order for a small company but, on July 2, just over a month later, TETRA was able to announce that it had signed a global marketing and development agreement with Halliburton. The fact that a company like Halliburton would team up with TETRA is a strong testament to the importance and potential reach of this unique product.

Once again, the best analysis of this event comes from Fluidsdoc, who wrote,

This confirms what TETRA has been telling us. There is work coming down the line for CS Neptune. It also strongly suggests that Hal[liburton] has a lock on some of this work [] and needed the tie-up with TETRA to supply a suitable non-zinc material.

This is enormously good news for TETRA. They have the “deal[,”] and have no need to discount to Hal[liburton] to secure the business. TETRA shares are going to rise as a result.

This gets back to something I said earlier. While management knows what’s going on better than anyone else, they obviously cannot disclose everything they know. But sometimes they can hint. For example, on the May 31 investor day, management stated that one of its goals was to “partner with [a] global drilling and fluids market leader” for the distribution of Neptune. Obviously, the deal with Halliburton was at a substantially advanced stage by then. In retrospect, management’s statement of strategy was more in the nature of a hint of what was to come.

So, when TETRA management writes, “The success of the Neptune technology project simply cannot be overstated,” and when they describe Neptune as “transformational, disruptive technology” what are they really trying to say? Is it a hope, an opinion, or a hint? I don’t know the answer, but given their recent track record, I’m open to the possibility that it may be a hint.

I also found Fluidsdoc’s next statement extremely interesting.

I have been involved in some of the industry discussions about how to respond to CS Neptune. As I discussed above, every major service company has been looking to create equivalent fluids technology. TETRA evidently has some pretty good patent lawyers, and a track record with Exxon Mobil, (XOM) in the GoM. The arms race is over, at least for Halliburton.

This is how I interpret this statement.

- “Every major service company has been looking to create equivalent fluids technology.” In other words, Schlumberger has been trying hard but, despite its considerable resources, has thus far been unable to duplicate what TETRA has done.

- Industry giants like Schlumberger need to figure out a “response.” In other words, Neptune presents a significant enough competitive threat to Schlumberger’s base fluids business that they cannot afford to just ignore it.

- Neptune is a patented technology and, it looks like their lawyers have sewn things up pretty tightly. Cf., Fluidsdoc’s August 18, 2017 article on TETRA where they wrote, “I'm not sure that CS Neptune is patentable or not; there just isn't enough information disclosed about it yet.”

- TETRA has a track record with Exxon Mobil in the Gulf of Mexico. Clearly, this “multi-billion-dollar investment well” in the Gulf of Mexico was with Exxon Mobil. I’m sure that’s pretty common industry information but, as an outsider, I did not know that. For ratification of an important new industry technology, you cannot get much better than that.

If you read carefully, there's a lot of good information there.

So, let’s return to my earlier question, how big and important is the market for CS Neptune? The answer is that it is big enough and important enough for Schlumberger and Halliburton both to have been seeking to develop a zinc-free drilling brine; and it is big enough and important enough for Halliburton to partner with TETRA when it found it could not duplicate its success. Remember, Tetra is not a large company and so it does not take all that much to move the needle here.

And what about Schlumberger? Fluidsdoc doesn’t say specifically, but notes,

Other companies [] may continue this race by trying to duplicate CS Neptune technology in a way that doesn't violate TETRA's patent. That has been going on for a while now, with no discernible results.

I read that statement to mean that Schlumberger is a long way from having a competitive product.

The Halliburton Marketing and Development Agreement

In the short term, the agreement with Halliburton will dramatically accelerate the global acceptance and reach of Neptune. That’s why I am excited about the stock in the short term. Once investors figure this out, the shares should start trading meaningfully higher. Remember, stocks anticipate.

Here’s the full text of the press release announcing the agreement,

TETRA Technologies, Inc. (NYSE: TTI) and Halliburton (NYSE: HAL), a global oil services company, today announced they entered into a global joint marketing and development agreement for the sale and distribution of TETRA's proprietary family of TETRA CS Neptune® completion fluids. The collaborative agreement also fosters and drives further development of other oil and gas drilling and completion fluids based on their respective technologies and resource capabilities.

"We are very pleased to have this agreement in place with a leading global fluids provider such as Halliburton. TETRA CS Neptune completion fluids are unique zinc-free, clear brine completion fluids that have significant potential for growth through global applications and as base fluids for other applications, such as packer and reservoir drill-in fluids. We look forward to working with Halliburton to expand sales and jointly develop new offerings," said Brady Murphy, President and COO of TETRA.

The agreement provides the opportunity for both parties to collaborate and utilize technologies and resources to bring innovative and efficient solutions to the market. A governance team comprised of technical and commercial members from each side will review proposed customer projects and make key decisions on resources and contributing technology to deliver approved projects.

"Halliburton Baroid is excited to add TETRA CS Neptune fluids to our market leading drilling and completion fluids portfolio," said Bradley Brown, vice president of Halliburton Baroid. "We look forward to collaborating closely with TETRA and our clients to utilize this technology in deepwater and complex high-pressure wells that require heavy clear brine solutions to control well pressure during the completion phase. Together we intend to further develop and apply the technology in innovative ways to help our clients maximize asset value."

(Emphasis mine.)

What’s important is that this more than a joint marketing agreement. It is also a joint technology sharing and development agreement.

On the second quarter conference call, the company gave further clarification on the both the short term and long term potential for this agreement.

Analyst: Okay, and then as you look out to 2019, can you maybe give us some insight in the conversations you're having with customers about potential Neptune projects in 2019?

TTI: Yes. I mean, as we mentioned TETRA had a pretty significant pipeline of projects that we have been in discussions with customers for some time over numerous geographic areas. Since the Halliburton agreement has been put in place, as I've mentioned, we have taken a subset of those opportunities where Halliburton has an infrastructure, a good footprint in place, customer relationships and have decided to prioritize on those particular projects. Some of those could materialize in 2019. Some of them are in 2019 and well beyond. These are long-range, mostly deepwater projects that we're identifying.

(Emphasis mine.)

But, as I said, the real opportunity is even bigger than that.

Analyst: I wanted to ask about the agreement with Halliburton. In that press release, there was some language about looking at potential new applications for the Neptune project—product that would utilize [it] as a base fluid for other applications. Could you maybe talk a little bit more about that? In particular, what would be the potential scope there?

TTI: Yes, Martin. So this is Brady. The agreement does address joint development opportunities where both parties bring technology to the table, and we jointly identified projects that we will work on together. As you know, Halliburton has a great drilling fluids business as well as a completion fluids business. And combined with our Neptune technology, there are some clear applications. One, in particular, would be reservoir drilling fluid. The drilling market is a huge market. There are benefits to having a clear brine fluid, like Neptune, as your base fluid, certainly, as it relates to impact on the reservoir while you're drilling. And so that would be one example of a project that we may look at. We have not initiated any development projects at this point. We're still in the discussion phase of what projects we'll prioritize, but that would be the one example with a potentially large application.

(Emphasis mine.)

As Fluidsdoc notes,

Both companies can now pool their resources to take full advantage of this opportunity globally. Brines are used not only as completion fluids, but have other applications as Murphy mentions in the press release.

The most significant of these is in the area of Reservoir Drill-in Fluids. These are used to drill the reservoir interval in open hole completions, to minimize damage while drilling. These are hugely profitable for service companies and drive a lot of ancillary sales.

(Emphasis mine.)

In other words, the joint agreement with Halliburton is really just the beginning. Expect to see more products based on the combination of Neptune and Halliburton technology. The potential for Neptune to be used as a base drilling fluid as well suggests the potential for dramatically higher volumes. If all of this bears fruit, I would not be surprised to see a more formal tie-up, such as between Schlumberger and M-I Drilling and, perhaps eventually, such as between Schlumberger and parent company Smith.

Financial Results and Guidance

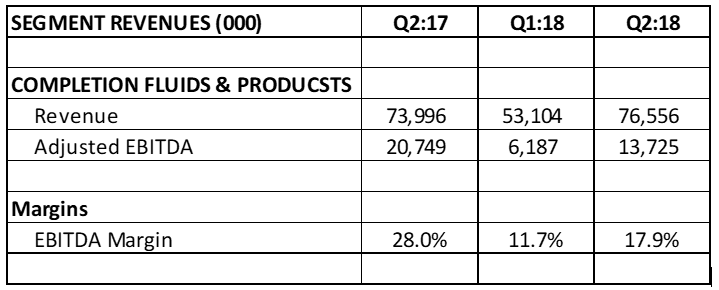

The fluids division had a really terrific Q2—much more terrific than it looked.

Source: Company filings, author's calculations

As can be seen, Q2 fluid revenue increased 44% sequentially and 3.4% year-over-year. While Q2 tends to be seasonally strong as a result of the European chemicals business, what’s notable is that results even increased year-over-year despite significant Neptune revenues in the year ago quarter and none in the current quarter. Without any contribution from Neptune, margins could not of course match the year ago quarter, but nevertheless they improved substantially on a quarter-over-quarter basis, rising from 11.7% to 17.9%.

One of the reasons that I am particularly excited about owning a full position in TETRA right here and right now is because I think that Q3 earnings will be stellar and Q4 guidance will be revised substantially higher.

To understand why, let’s take a look at the company’s investor day guidance for the fluids division. Source: Company filings, author's calculations

Source: Company filings, author's calculations

As can be seen above, I have recorded the company’s full-year 2018 guidance in blue and the actual results for the first two quarters in black. In red, I have calculated what each quarter would look like to meet the mid-point of guidance. (For the sake of simplicity, I have assumed that both quarters would be identical.)

At the investor day, the company confirmed then full-year revenue guidance for the entire company of $945-$985 million. In fact, this guidance was actually first introduced on the company’s Q1 conference call. What was new at investor day was the breakout of revenue guidance by division. Thus, we can assume that, had the company given the divisional breakout on the Q1 conference call, it would have been mostly the same as what they gave on investor day.

Now, here’s where it gets interesting. On the first quarter conference call, management stated,

Commercial discussions are well advanced on several CS Neptune opportunities. We remain confident that one to two of these projects will materialize and have a significant impact on our results in the second half of this year.

(Emphasis mine)

Neptune revenues are so large and consequential that I cannot imagine other than that, if management thought there might be “one to two” opportunities, they would only incorporate one into their formal guidance. To do otherwise would risk falling materially and embarrassingly short of guidance, something I am sure management did not want to do out of the box.

But, on the second quarter conference call, management stated that it now expects revenue from two Neptune wells during the second half of the year.

The second data point, as we talked about the status of the two Neptune projects we’ve been discussing these past several quarters and expect to execute those and collect the cash this year. One of those, we said was at a fairly advanced stage in the drilling process.

The company also stated,

During the third quarter, we’ll revisit the TETRA projections as we offset any potential impact from the Permian Basin concerns and the formal award and timing of the CS Neptune projects previously discussed.

In other words, it seems that current guidance for the remainder of 2018 only includes one Neptune well, but there is a significant likelihood of a second such well. Given that one was already at a “fairly advanced stage in the drilling process,” it’s possible there will be meaningful Neptune revenues in Q3. If so, Q3 could be surprisingly strong and there could be a surprisingly substantial upward revision to Q4 guidance.

WATER & FLOWBACK SERVICES DIVISION

The second important division at TETRA is their Water & Flowback Services division which provides water services for unconventional wells in North America.

The leader in this business is a company called Select Energy Services, Inc. (WTTR), and I have written extensively about why I think water handling and logistics is a very much underappreciated business with strong growth prospects and durable margins.

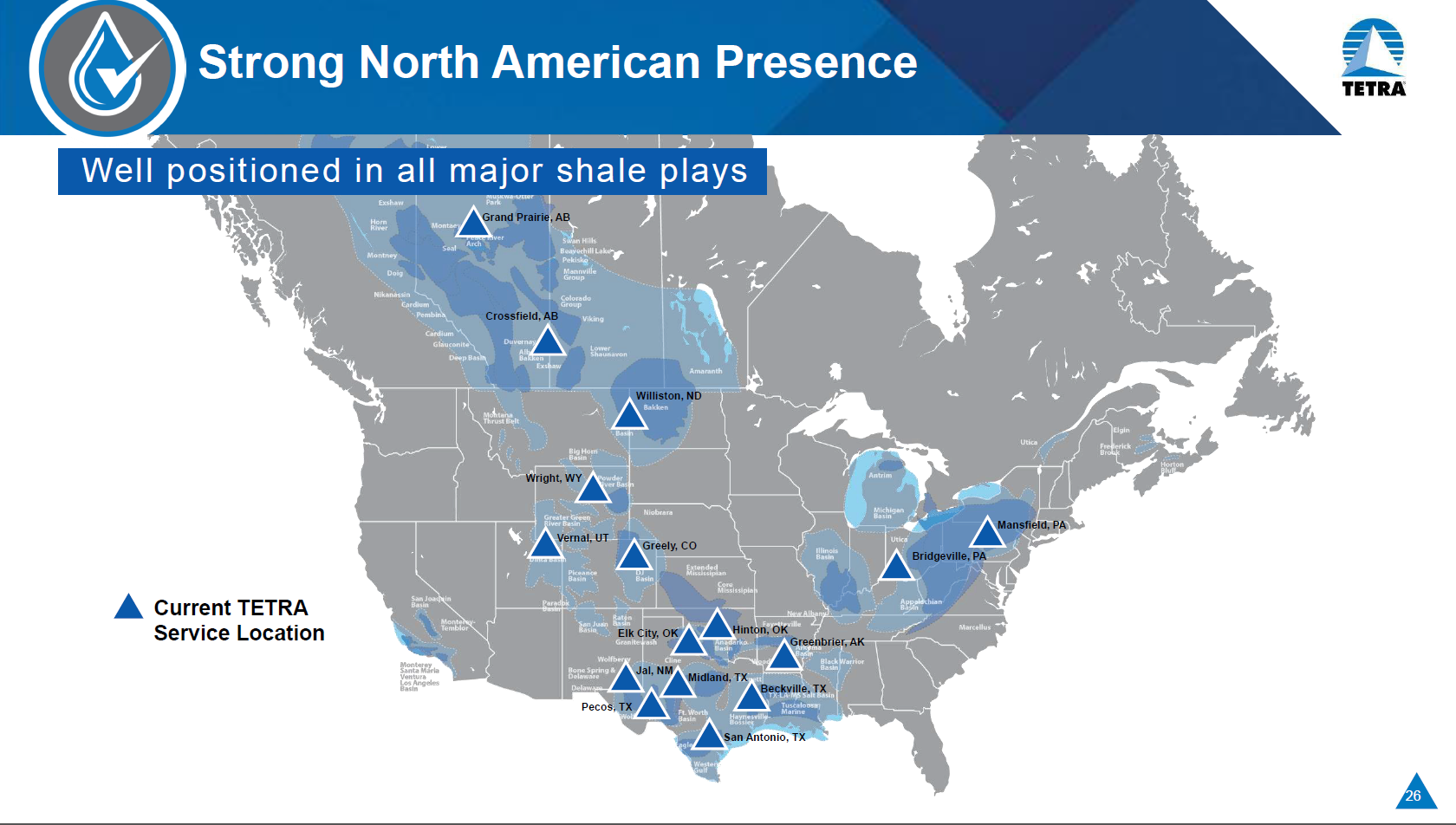

TETRA is number two in the water business. While considerably smaller than Select, they also have a national footprint with operations in all the major shale basins. As far as I know, all the other players are regional.

Source: Company presentation

Source: Company presentation

Since TETRA’s water business is, for the most part, very similar to Select’s, I am not going to reiterate what I have written previously. Suffice it to say that water handling and logistics is an increasingly important and mission critical component of unconventional well completions and Select and TETRA are the two publicly traded companies with a national footprint. Readers are urged to read my first two articles on WTTR for more details about this business and why I think it will grow significantly over the next few years.

In March 2018, TETRA doubled down on its water business by purchasing Swiftwater for $42 million in cash and 7.772 million shares of stock valued at $28.2 million. This was an excellent acquisition which gives them a substantial market position in the all-important Permian Basin.

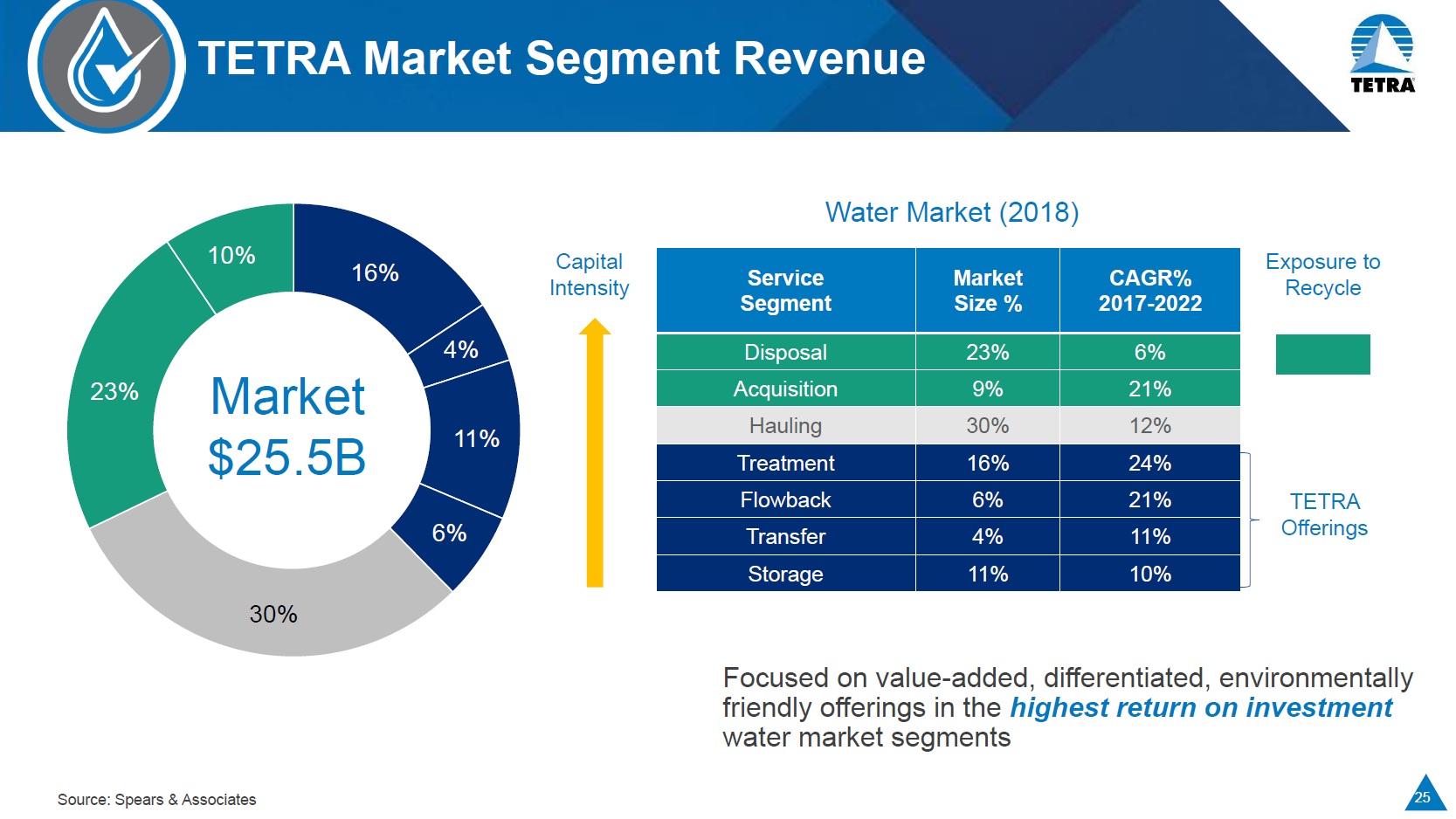

Currently, TETRA is exposed to the $9.4 billion market for the treatment, flowback, transfer and storage segments of the water business, all of which have substantial growth prospects over the next few years. The company’s objective is to deliver double the growth rate of the industry, which would suggest well better than 20% annual growth.

Source: Company presentation

Source: Company presentation

One reason I like the water business is because, in addition to the strong growth prospects, it also generates very significant free cash flow.

Source: Company presentation

Source: Company presentation

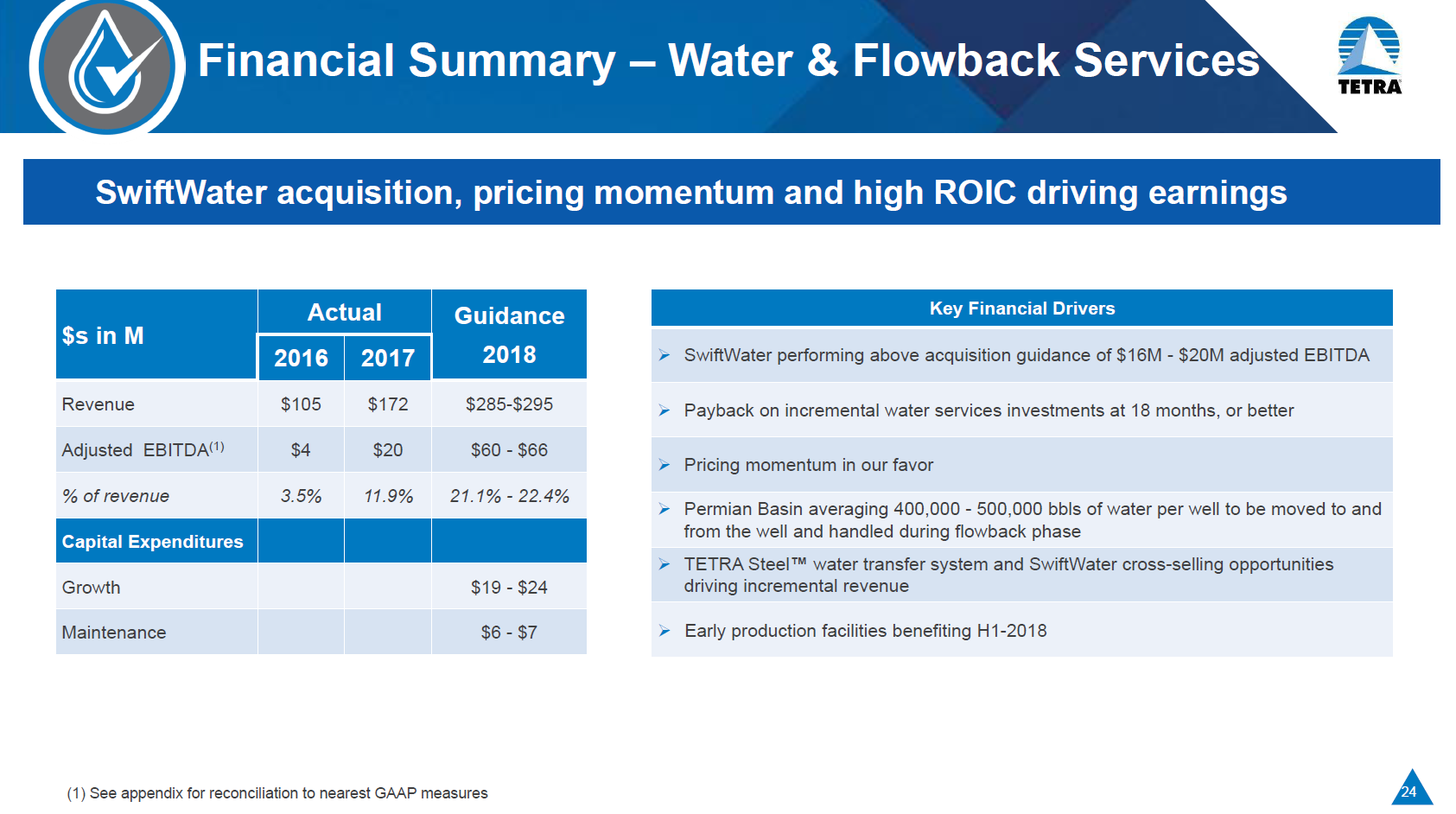

As can be seen above, TETRA management is forecasting EBITDA of $60-66 million for 2018 (a number which is likely quite low) against which it has maintenance capex of just $6-7 million. That bespeaks a very high quality of earnings. Management is further investing another $19 to $24 million in growth capex, on which it expects to earn a payback in 18 months or less. That suggests strong EBITDA growth into 2019 and 2020.

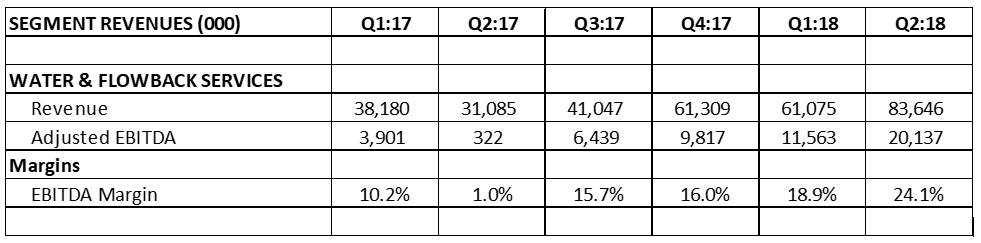

Financial Results and Guidance

One thing I’ve come to appreciate about management is that they have given very conservative guidance that they have then handily exceeded. For example, at the time of the Swiftwater acquisition in March, they estimated that Swiftwater would contribute $16-20 million in EBITDA for 2018. Swiftwater has already generated EBITDA of $2.3 million for March and $6.8 million for Q2, the first full quarter.

As can be seen, water division revenues have been growing significantly and EBITDA margins have improved significantly as well.

Source: Company filings, author's calculations

Source: Company filings, author's calculations

While the better part of the growth from Q1:18 to Q2:18 was due to the added two months of Swiftwater revenues, the segment did enjoy significant organic growth as well. On a pro forma basis, assuming Swiftwater had been acquired at the beginning of the first quarter, Q2 water revenues would have grown by 11.2% sequentially. Note also the tremendous margin improvement that the acquisition of Swiftwater has enabled.

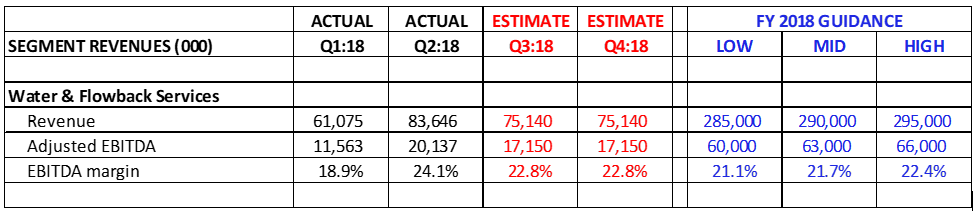

At the analyst day, management gave guidance for full-year water revenues of $285-295 million and $60-66 million in EBITDA. With the Q2 report now in hand, even the top end of that guidance seems woefully low. Source: Company filings, author's calculations

Source: Company filings, author's calculations

As can be seen above, assuming the top end of the revenue and EBITDA guidance, results for Q3 and Q4 would have to fall very substantially below the Q2 run rate. I don’t think that’s likely. I think it is more likely that EBITDA guidance will be ranged from $60-66 million to perhaps $70-75 million.

On the Q2 conference call, one analyst addressed this issue.

Analyst: Just a quick question drilling down on guidance on the full-year. So like, for example, on water, if your second half results were just flat from 2Q levels, [you would report] $72 million in EBITDA [while] guidance is standing at $60 million to $66 million. Any color there would be helpful. Is this just caution over what Permian activity is going to look like? Or what [] drove you guys not to revisit that guidance today?

TTI: So Jake, good question. We did have a really solid quarter on the water and flowback testing side. Brady talked about picking up some integrated projects that we think, would have upside opportunity. We’re going to take a cautious approach, reassess during the quarter to make sure that the impact of any other takeaway concerns don’t impact our outlook. And then, when we report the next quarter, you’ll see us address the opportunity to continue the profitability with the water management and flowback testing.

Analyst: Okay. So fair to say a bit of conservatism just baked into it?

TTI: Fair to say that.

Analyst: Okay. And then secondly, if I look at Swiftwater sort of the growth rate relative to—if you just annualize their—or gross up the 1Q result, looks like it's growing at about 18%, but that implies kind of a materially lower growth rate in the legacy business. I was wondering if you could just give us a little bit color. What's going on there?

TTI: The legacy business is holding its own. It's doing well. One of the benefits that we're seeing is that the customer base that came across with Swiftwater didn't have access to TETRA STEEL double-jacket, lay-flat hose. So we're moving a lot of our service offerings and technology in this area and benefiting the customer base that So keep in mind that this is a collaborative TETRA-Swiftwater customer base product offering, employee base is supporting both. And as we get further into the integration, it's going to be harder to segregate one versus the other because we're starting to move people, equipment and assets back and forth. And it's a matter of, do you assign a TETRA STEEL project to an existing opportunity brought forward with a Swiftwater customer base or pursue a completely new opportunity? As we reported in the future quarters, it'll be hard to distinguish what is Swiftwater versus TETRA because we're integrating it significantly.

TTI: And just to add to that, Jacob. Again, I think, one of the points we want to get across is, in addition to the strength in the Permian, we've seen strength in the other basins, which is very encouraging. And within that construct, we've seen continued strength in margin enhancements on the testing side. We've said over the last year that we thought the domestic testing margins would lag the water progression, and I think it has. But we're starting to see, as we said on the call, margin starting to move back to where they were back in 2014. So we're very encouraged about that progression as well.

(Emphasis mine.)

In my opinion, this sounds like a company that is going to meaningfully raise its guidance for this division when it reports Q3 earnings.

COMPRESSION SERVICES

TETRA’s third important division, Compression, is not so much a division as an investment in a separate, publicly traded company known as CSI Compressco, LP (CCLP). Compressco is a vertically integrated compression company, meaning that they supply compression services, but they also manufacture, sell and support their own equipment. They also provide aftermarket support for third party equipment.

For the most part, compression is a mildly cyclical business that fluctuates with oil and gas prices and offers rent-like returns. It is a heavy iron business, requiring lots of assets that are optimally financed by low-cost debt. Currently, this business is coming off the bottom of the cycle and management has done some smart things. First, they paid down their bank debt and issued senior notes, also adding $100 million to their cash balances in the process. The company is now in a comfortable position with no covenants and no debt coming due until 2022 at the earliest.

Then, management used this additional money to invest in increasing their available horsepower. Utilizations have rebounded significantly off the bottom and Compressco’s earnings and dividend are set to move higher.

Source: Company filings, author's calculations

Source: Company filings, author's calculations

Unlike most of its peers, Compressco is vertically integrated and manufactures its own equipment and provides aftermarket support for its own and third-party compression equipment. As utilization has rebounded, the compression market has gotten tighter and there has been increasing demand for both new equipment and aftermarket service. At June 30, 2018, the company reported the highest backlog in its history, $102.2 million, which reflects an order from a single customer for $67 million—the largest such order in their history. By comparison, its backlog at the year ago period was just $24.0 million. Most of this backlog is expected to be delivered in the second half of 2018, so expect a significantly stronger second half. Whether the company can continue this momentum remains to be seen.

Bottom line, the compression division is in a good place. When management raised guidance on the Q2 conference call, it was entirely attributable to this division. It may not be the most exciting business, but it is headed higher

Accounting Considerations

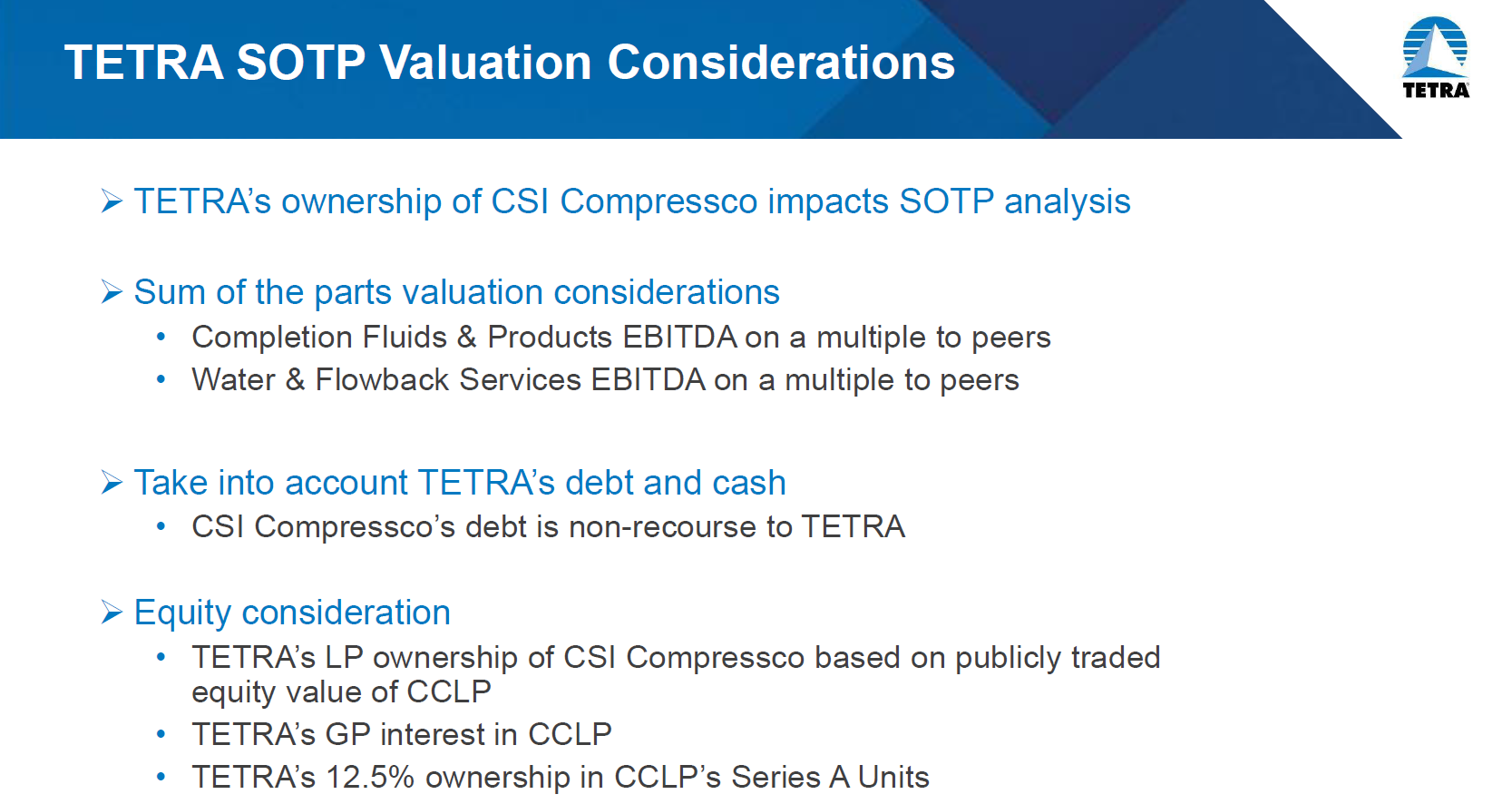

Now, this is where things get a little complicated from an analytical standpoint. Essentially, Compressco is its own company (structured as an MLP) and at the last report TETRA owned about 37% of the common LP units, 12.6% of the preferred units and an approximately 1.6% general partner interest. In many ways, TETRA’s interest in CCLP is more in the nature of an investment than a true operating subsidiary. Like any other common holder, it benefits primarily from an appreciation in the value of CCLP stock and any dividends paid by CCLP. Other than that, CCLP is a financially and legally separate entity and there is no commingling of cash or cash flows. To the extent that TETRA owns less than 50% of CCLP, it would normally account for its interest as an equity investment. But, because TETRA also owns the general partner interest, it exerts functional control over CCLP and must therefore consolidate CCLP’s financials with its own. This makes the analysis of TETRA’s financials a bit messy.

What do I mean by messy? If you look at TETRA’s most recent balance sheet, you’ll see $810 million of long term debt. The reality is that $632 million of that debt belongs to Compressco and, while TETRA must include that debt on its balance sheet, it is in no way liable for that debt under any conditions. Basically, TETRA owns about a 40% economic interest in Compressco and the best way to think of this is that TETRA’s interest is mostly like that of any common unit holder. But because TETRA must consolidate the financials of CCLP with its own, they seem much more intertwined than they really are.

Valuation of Compressco

I believe that, notwithstanding TETRA’s effective control over CCLP, its interest should be valued primarily as a standalone equity investment. Therefore, this is how I value TETRA’s interest in CCLP.

• At June 30, 2018, TETRA owned 15,428,587 common units of CCLP. At their last traded price of $5.48, this stake is worth $84.5 million.

• TETRA also owned 559,975 shares of CCLP’s Series A preferred units. Over the next year, these shares will convert ratably each month into common units of CCLP. I value these at par, or $5.6 million.

• In addition to exercising function control over the company, the general partner interest in CCLP is entitled to 1.6% of CCLP’s dividend payments plus incentive distribution rights as dividends rise beyond a certain level. Beyond the value of the dividend distributions, the value of the general partner is somewhat difficult to establish. The incentive distribution rights are too far out of the money to be a meaningful source of value, but control is worth something. Thus, I am going to somewhat arbitrarily value the general partner at $0 to $30 million. The upper end of that range presumes that TETRA will use its control to monetize its investment in CCLP at a premium, perhaps by selling the company outright.

All told, I value TETRA’s interest in CCLP at $90 million to $120 million, most of which is the current market value of its securities holdings in the company.

While nominally the largest of the three divisions by both revenue and EBITDA, I believe Compression is actually the least valuable division. It is also likely creating value at the lowest rate compared to the other divisions. I believe its relative value to TETRA will rapidly diminish in importance as compared to the fluids and water divisions. According to the company, there are cross-selling synergies with its other divisions; but I’m just not sure that they are sufficient to warrant keeping the division given the complexity it adds to the capital structure.

Compressco is poised to do better and I think that management should use this as an opportunity to monetize their investment. While they could always sell their shares into the market place, the value of having control is they could also sell the company to a third party, likely at a premium. In my opinion, Compressco should be sold because TETRA now has bigger and better fish to fry. Given its control position, why not seek to obtain an acquisition premium?

BALANCE SHEET

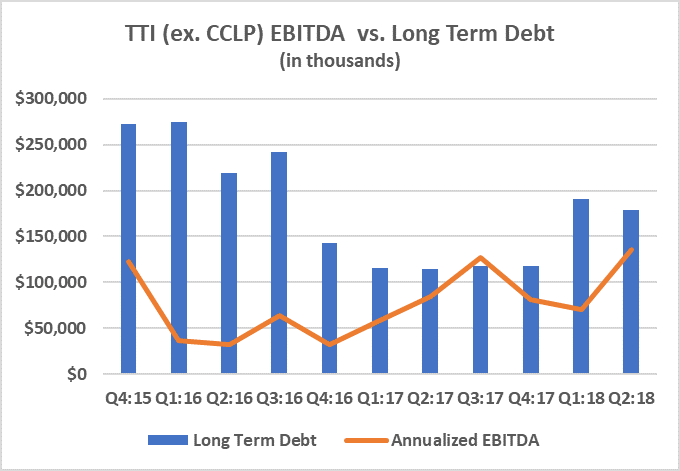

An important part of TETRA management’s remake of the company has been to clean up its balance sheet. Currently, TETRA has $178 million of debt versus its most recent quarterly EBITDA of $33.9 million.

Source: Company filings, author's calculations

Source: Company filings, author's calculations

A sale of CCLP could reduce its debt by at least half or more, freeing up capital which could be invested in either of its two other divisions.

VALUING TETRA

Before I discuss how to value TETRA, let me discuss how not to value it. Many analysts are valuing the company on a consolidated basis, that is, assigning a unitary target multiple to a consolidated EBITDA figure including Compressco. I don’t think that’s right because each of the company’s three divisions are really quite different in terms of growth prospects, capital intensity and risk. The compression division, in particular, is a horse of a different color. Notwithstanding the consolidated financial presentation, there is no commingling of assets, liabilities or cash flows between TETRA and Compressco, and so it is essentially improper to value them on a consolidated basis. Furthermore, in almost all cases, this unitary multiple is far too low because it does not consider that Neptune is a very large and high multiple product opportunity.

I believe the company agrees with me that the correct way to value TETRA is a sum of the parts analysis with the value of Compressco “mapped over” from its public valuation.

Source: Company presentation

Source: Company presentation

So, here’s how I value TETRA on a sum of the parts basis.

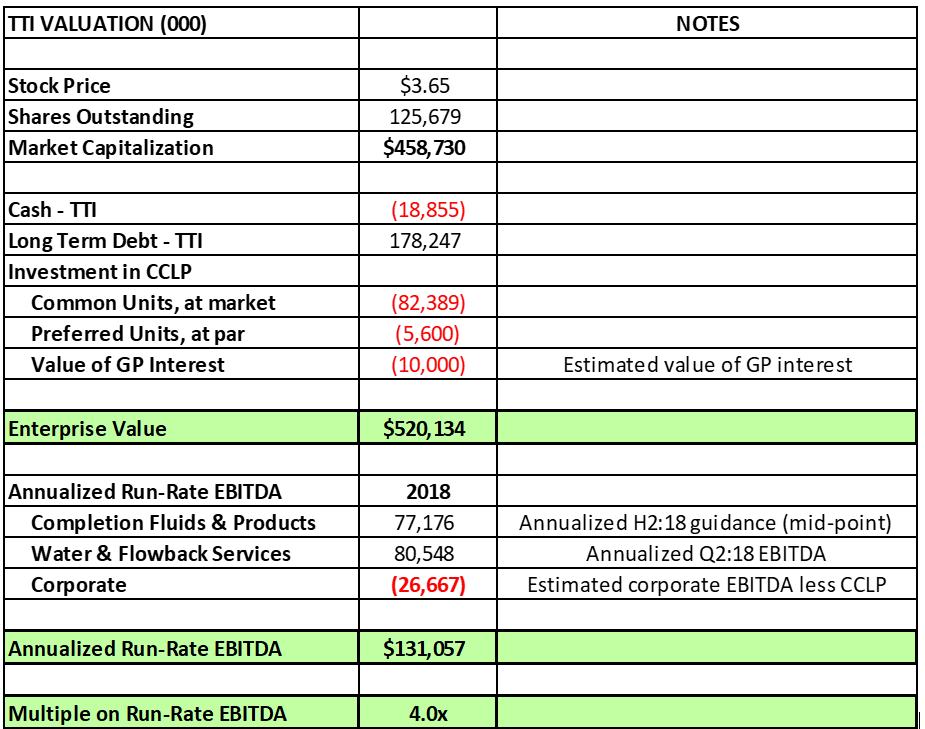

Current Valuation

In order to establish a current valuation, I try to establish a reasonable current EBITDA run rate for the fluids and the water divisions. For the fluids division, I use the midpoint of management’s guidance less the reported first half results to establish a current run rate. For the water division, I use the Q2 actual run rate. I believe that both are likely conservative.

Source: Company filings, author's calculations

Source: Company filings, author's calculations

As shown above, this yields an enterprise valuation of approximately 4.0x the current run-rate EBITDA. That’s a very attractive valuation for a company that is both generating significant free cash flow yet also has bright growth prospects.

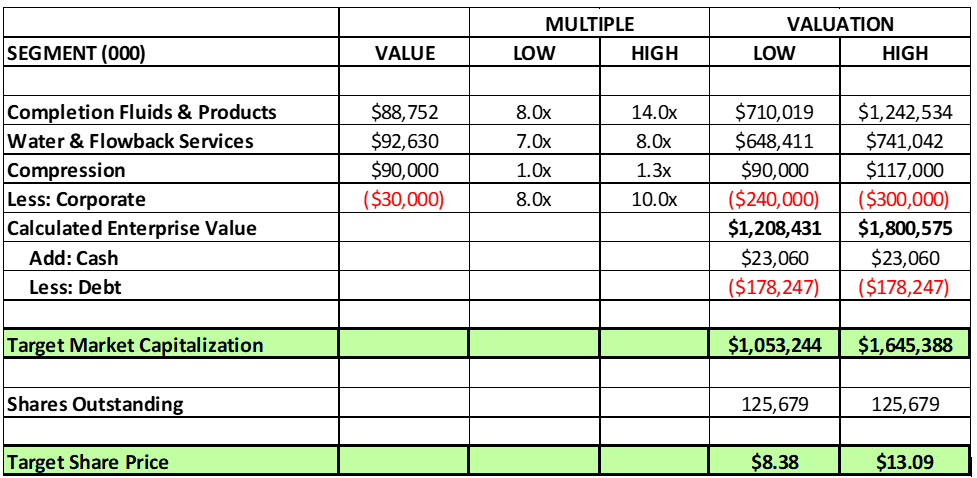

Target Valuation

Given that the calendar is pushing November, TTI should really be valued on 2019 cash flows. Since management hasn’t given guidance for 2019, I will need to provide my own. I expect that I will have a much better handle on the potential for 2019 by the Q3 earnings call, but for now I will simply grow the run-rate EBITDA by 15% for each division. I think each division is easily capable of significantly exceeding those placeholder estimates.

Thus, on the low side, I think the compression division is worth $90 million, which is the market value of TETRA’s ownership position plus the value of its GP dividend interest. On the high side, I think you can add a 30% premium in a change-in-control scenario, resulting in a value of $120 million.

As I noted in my articles on WTTR, this is a good business with good growth prospects, modest reinvestment requirements and robust free cash flow generation. It is a better and less capital intensive business than pressure pumping and a very much better business than frac sand, which is now beset by significant oversupply issues. On balance, I think the Water & Flowback Services division is worth at least a 7.0-8.0x multiple. This yields a valuation of $648 million to $741 million for this division.

The Completion Fluids & Products division is the most difficult to value because of the significant potential for Neptune. For now, I am going to value it at 8.0-14.0x the mid-point of current H2:18 EBITDA (the result of subtracting actual H1:18 EBITDA from full-year mid-point guidance of $58.5 million and then annualizing). I understand that’s a bit of a wide range and that a 14x multiple may seem a bit on the high side. But, if Neptune can fulfill even half of its potential, this will seem a very modest valuation in a year’s time. That yields a total value of between $710 million and $1.2 billion for this division. Source: Company filings, author's calculations

Source: Company filings, author's calculations

Adding it all up and adjusting for corporate overhead yields a valuation range of between $8.38 and $13.09. Even the low end of the range is more than a double from these prices.

Most of the variation in the valuation comes from the prospects for Neptune. The low end of the valuation range reflects an outcome in which Neptune never amounts to much more than a niche product, used in a handful of wells each year. The upper end of the valuation range assumes meaningful penetration and growth for the product. Remember, Neptune is a groundbreaking product in its infancy with drug-type margins, patent protection and, thus far, no competition. A single Neptune project contributed almost $25 million of revenue and $20 million of EBITDA in less than two full quarters. With two Neptune projects scheduled for the second half, the real question is what can 2019 and 2020 and 2021 produce in terms of Neptune earnings. If the agreement with Halliburton bears significant fruit, even the high end of the valuation range will ultimately prove far too low.

CONCLUSION

I believe investors should buy TTI now, ahead of the Q3 earnings report. Even at the lower end of my valuation range, which assumes that Neptune never becomes more than a niche product, the stock can double. If I am right about the prospects for Neptune, this stock can trade in the mid-to-high teens soon enough.

Disclosure: I am/we are long TTI WTTR.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

-

1

1

1 Comment

Recommended Comments